The insect farming industry has a £100 million problem. Actually, make that closer to £2 billion. That is the rough figure that venture capital poured into large-scale insect protein factories over the last decade — and most of it is gone.

Ÿnsect, Agriprotein, Hexafly, ENORM. The list of high-profile collapses keeps growing. And behind the scenes, even some of the so-called “survivors” are looking shaky. I’ve been researching this field since 2013 and working inside it for six years as CEO of Flybox. What you’re getting here isn’t hype. It’s the view from the trenches.

If you’re writing an insect farming business plan today, understanding why these giants failed is the most important thing you can do. Because the failure wasn’t bad luck. It was structural. And if you repeat their model, you will repeat their outcome.

The Gold Rush Mentality That Broke the Industry

To understand the collapse, you have to start with human psychology — specifically, the predictable gold rush mentality of agricultural innovation. Someone discovers a natural process that looks like it could save the planet. Investors get excited, founders get funded, and soon there’s a mega gold rush.

In the case of insect farming, the logic was seductive. Insects are nature’s recyclers and a rich source of protein. Farm them at industrial scale, turn waste into feed — circular, sustainable, brilliant. And in principle, yes, it is brilliant. But in practice, economically, it has been a disaster.

This same boom-and-bust cycle has played out across every agricultural tech wave: lab-grown meat, vertical farming, plant-based proteins, land-based aquaculture. The pattern is always the same. A compelling narrative drives capital in, valuations get way ahead of unit economics, and then the scaling reality hits. The trough of disillusionment is deeper and longer in biological systems than in software because biology and food value chains move slowly. The lag from hype peak to rational scale is typically five to ten years.

The insect farming hype peaked around 2021. We are now in the trough. The question is: what comes next?

Why the Protein-First Model Was Always Broken

The core failure of Generation 1.0 insect farming was a fundamental misread of the market. These companies built their entire business model on selling premium insect protein. That was the fatal error.

Consider the commodity reality. Soy meal trades at roughly $500 per tonne. Poultry meal at $700 per tonne. Fish meal at $1,500 per tonne. Insect protein in Europe? $3,000 to $4,000 per tonne. You cannot expect feed mills, pet food producers, or aquaculture companies to pay two to four times more without an overwhelming reason — and the research simply did not justify that premium at scale.

The early players tried to claim that insect protein was superior for animal health and the environment. Some of that research is genuinely interesting. But most of those claimed benefits can be achieved through cheaper ingredient blends. The industry pushed the narrative far harder to attract investors than to actually win over buyers.

What actually happened was this: large aquaculture companies, under pressure from investors and regulators to decarbonize, were willing to pay a green premium temporarily — just to test the claims and tick the ESG box. It was a drop in the ocean compared to their total protein spend. Once their trials ended and the economics didn’t stack up, the subsidy stopped. And the collapse started.

That is not a market. That is charity with an expiry date.

The Engineering Trap: Building Rolls-Royces for a Ford Focus Market

The second catastrophic failure was the CAPEX obsession. Generation 1.0 facilities were engineering showpieces — intricate robotic tray systems, automated crate stacking, plenum climate control delivering precise conditions to every individual tray level. Beautiful. Expensive. Economically indefensible.

The capital expenditure for these facilities often exceeded $100 million. Some went far higher. To guarantee consistent protein output, many also relied on purpose-grown grains or high-quality feedstocks rather than true organic waste — meaning they were paying for their inputs rather than being paid to take them.

This created a fatal economic paradox. The cost of production — driven by massive CAPEX depreciation, high energy costs for climate control, and expensive inputs — pushed the break-even price of insect protein well above £3.00 per kilogram. The market clearing price was under £1.50. When your cost of production is double what the market will pay, no amount of scale or automation can save you.

To summarise why Western factories failed:

- They focused on premium protein instead of starting from waste management

- They massively over-capitalised — building trophy architecture when pragmatic engineering would have done the job

- There was no true product-market fit — only a temporary green premium dressed up as scalable demand

- They scaled too fast before proving the fundamentals at pilot scale

The IWM Model: Waste Is the Product, Insects Are the Byproduct

The collapse of the protein-first model does not mean insect farming is dead. It means the business model has to evolve. And the evolution is already underway.

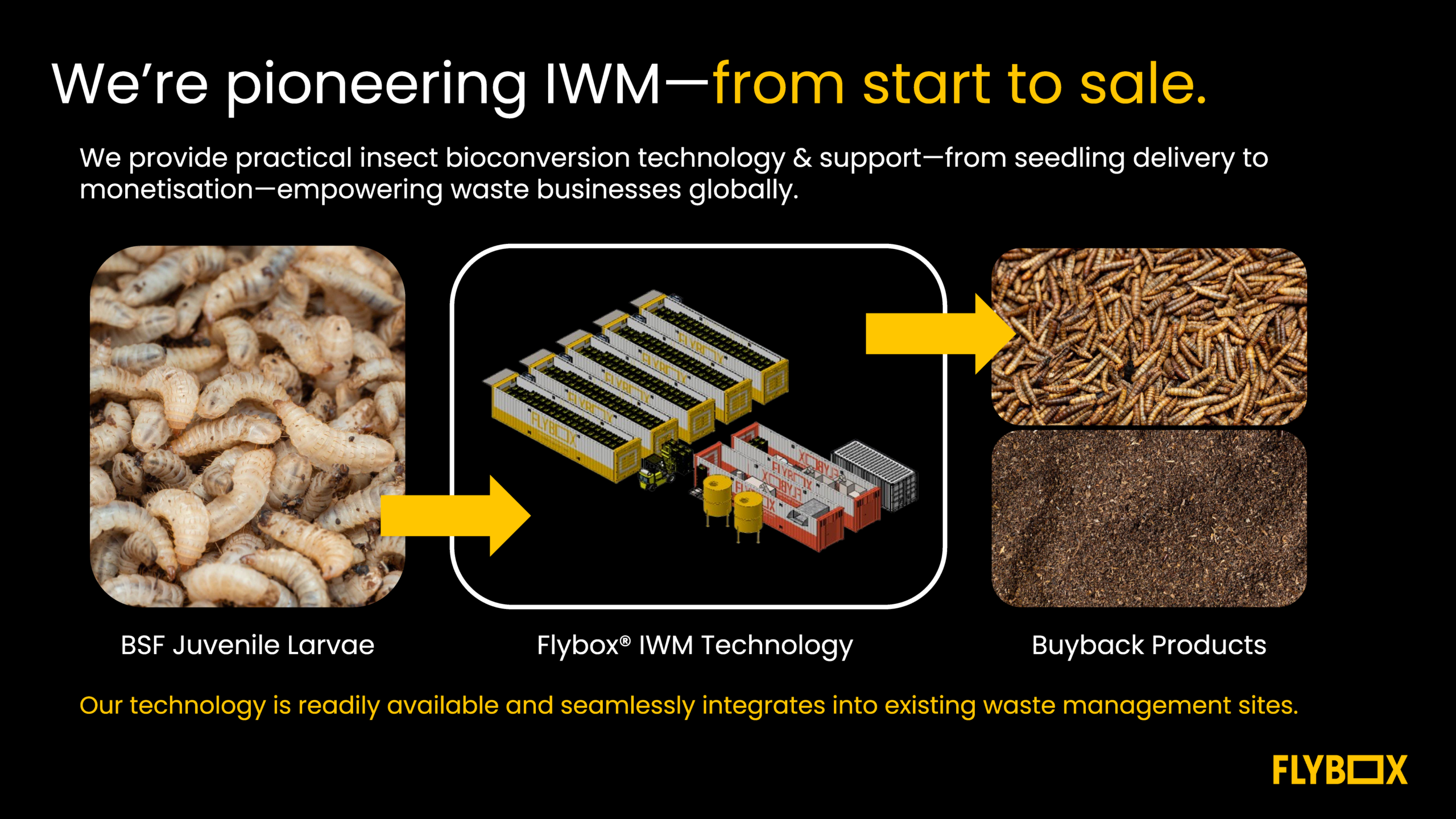

The solution is a fundamental repositioning of the value proposition: from producing premium protein to providing essential waste management services. This is the core of what Flybox calls Insect Waste Management — IWM.

In the IWM model, a primary revenue driver becomes the gate fee — the price paid by a waste generator to dispose of their organic waste. Food manufacturers, supermarket distribution centres, agricultural producers — they all have organic waste problems that cost money to solve. An IWM operator gets paid to take that waste, process it through Black Soldier Fly bioconversion, and return value-added products.

- Stable, contract-based revenue: Gate fees are insulated from commodity protein market volatility. You are in the waste management business, not the protein commodity business.

- Negative-cost inputs: Instead of paying for feedstock, you are paid to take it. This single shift transforms the unit economics of the entire operation.

- Byproduct bonuses: The resulting BSF protein, oil, and frass fertiliser become bonuses on top of a stable waste-processing income — not the sole mechanism for survival.

This model also aligns the insect farm with powerful regulatory tailwinds. The UK’s Simpler Recycling scheme came into force in 2026. The EU’s organics-to-landfill ban hits in 2030. Anaerobic digestion plants are already flooded and starting to charge double what they did three years ago. Waste managers are desperate for new solutions. IWM fills that gap — fast to deploy, no grid connection required, handling the waste streams that other technologies ignore.

What Generation 2.0 Engineering Actually Looks Like

Shifting from a protein-first to a waste-first model requires a fundamental reimagining of insect farming engineering. Generation 1.0 facilities prioritised biosecurity and feed conversion ratios. Generation 2.0 facilities must prioritise throughput and capital efficiency. This may mean they are less suited to some regions than others, but this is the reality f where we stand today.

When the goal is to process as much waste as possible, as cheaply as possible, the intricate robotic tray systems of the past become a liability. The future belongs to modular, continuous, high-velocity industrial processing.

This is where the Flybox Container System and Flybox Factory System come into play. By focusing on modularity, robust proprietary climate control algorithms, and high-density rearing, these systems drastically reduce the CAPEX per tonne of processing capacity. A traditional Western robotic tray system might cost £100k – £200k per tonne of capacity. A pragmatic, throughput-focused modular system can achieve the same capacity for £40,000 to £80,000 per tonne. That lower capital burden directly translates to a shorter payback period and a viable ROI or lower insect protein prices.

The IWM model also solves the logistics problem that killed many of the early players. Logistics costs can account for up to 40% of the total cost of insect protein in a centralised mega-factory model. By deploying modular technology directly on waste sites, you eliminate that cost entirely. The waste doesn’t travel. The technology goes to the waste.

Breeding and entomology in the IWM model also becomes a service. Specialist companies supply new operators with a steady stream of juvenile larvae. This means smaller-scale sites can actually make commercial sense — start small, validate the model, scale gradually, integrate directly within existing waste operations. No £100 million bet required.

Newer technologies that move past the Robotic arm systems developed in Asia significantly reduce the operating costs wit more efficient channeling of larval metabolic heat and and lower labour utilisation.

Building a Viable Insect Farming Business Plan Today

Secure the waste contract first. Your most important asset is not your technology. It is your waste agreement. Identify a specific, quantifiable organic waste problem — a food manufacturer generating 50 tonnes of fruit and vegetable waste per week, a brewery with spent grain, a supermarket chain with unsold produce. Secure a gate fee. That is your revenue foundation.

Minimise CAPEX and validate before scaling. Do not over-engineer. Choose modular, scalable technology that allows you to prove your model at pilot scale before committing serious capital. A £150,000 to £500,000 R&D or pilot facility should answer every critical question about your feedstock, your bioconversion rates, and your local offtake markets before you commit to a £1m to £5m commercial build.

Develop local offtake for your products. Do not rely on global commodity markets for your protein and frass. Find local buyers — aquaculture producers, pet food manufacturers, horticulture businesses — who value the sustainability and circularity of your product and will pay a modest premium for it.

Think live insects, not just processed protein. The most defensible end product in the insect farming industry is the live insect itself. Fish, chickens, and pigs are biologically tuned to seek out insects. Live insects improve welfare, regulate negative behaviours, and deliver measurable performance benefits that no processed ingredient can replicate. Nothing competes with an insect except an insect.

The Industry Is Not Over. The Old Model Is.

I still believe insects can become one of the pillars of a truly circular food system. That is why I get up in the morning. But first, we have to be honest about the mess before we can get to the solutions.

The era of mega-factory insect farm VC funding is over. Paradoxically, that is the best possible thing for the long-term health of this industry. Capital will now come from corporates in waste, food, and agriculture — strategic investors who understand the value of a closed-loop system and are not chasing a 10x return in three years. Prezero has already acquired Agriprotein’s IP. Tesco is testing insect-based pilots. Waste companies in the UK and Asia are quietly moving in.

The second generation of insect farming companies — the ones building on the mistakes of the first — will be leaner, more pragmatic, and more focused on solving real waste problems for real customers. They will not be building Rolls-Royces. They will be building workhorses t the forefront of efficient heat distribution and waste management.

That is the right way to start an insect farm. And it is the only model that will still be standing in ten years.

Ready to build a viable IWM operation? Book a consultation with the Flybox team to discuss how our modular technology can transform your organic waste liability into a profitable, contracted revenue stream.